Some of the numbers presented in this website may not be the most recent available

globalshift.co.uk - copyright © 2009 to 2026; All rights reserved

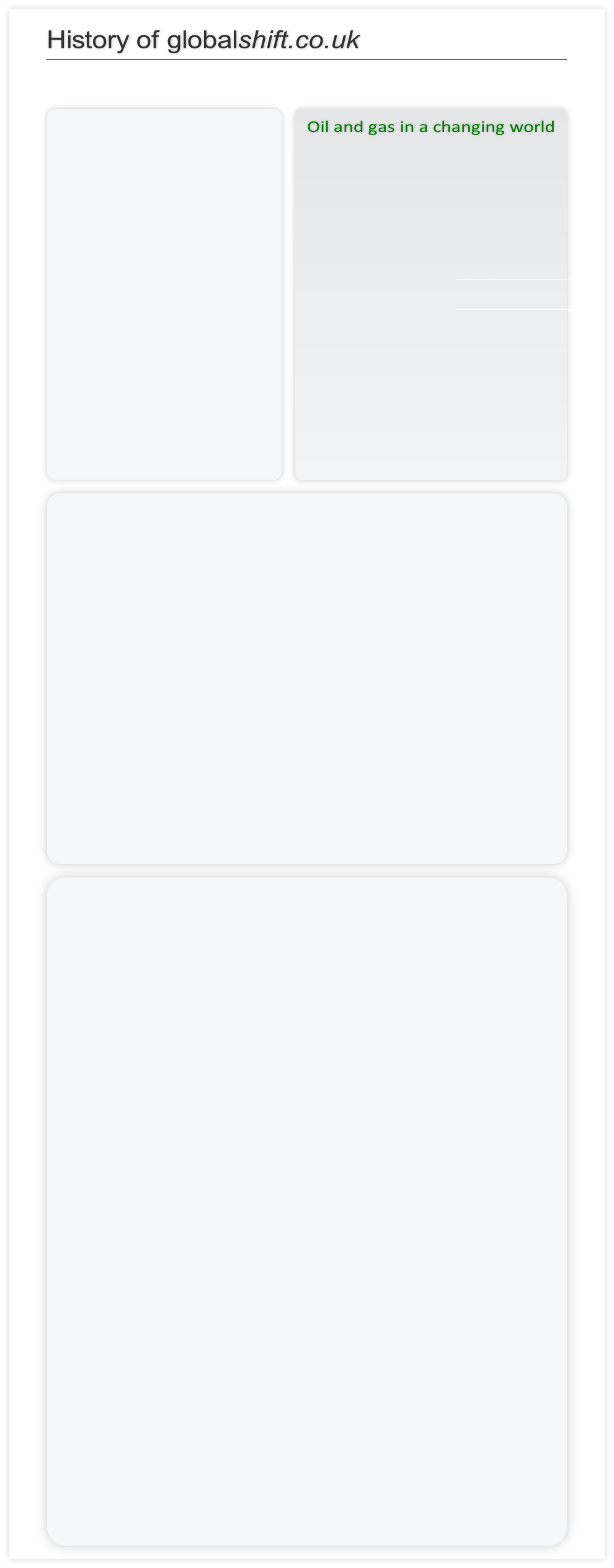

THEN

Oil finders

Specific Services

Specialisation

Traditional

Technical Solution

Vertical Drilling

Reactive

Exploration Focus

Competition

People

Manual

Research

Secrecy

Exploitation

Supply

GROWTH

NOW

Business Executives

Integrated Providers

Multi-discipline

Unconventional

Cheapest Solution

Horizontal Drilling

Proactive

Development Focus

Co-operation

Artificial Intelligence

Remote

Practice

Information

Environment

Demand

DECLINE

Dr Michael R Smith

Michael has worked in the oil industry, consulting on energy policy and strategy since 1982.

He received his doctorate in geology from Oxford University and spent the early years of his career as a consultant based in Asia. He went on to work with a number of oil companies as a geoscientist, and later, as an Exploration Manager.

Michael incorporated Energyfiles in 2003, turning it into a renowned source of energy data. After selling the company in 2009 he developed new ideas on energy supply and demand, creating globalshift.

He has worked on E and D projects in nearly every region of the world and has lived in Europe, The Middle East and Asia.

globalshift.co.uk

Globalshift.co.uk was at first an energy advice site but now provides oil and gas forecasts and information relevant to the ‘Energy Shift’ (see below) to the oil and gas industry, alternative energy suppliers and users, and other interested parties.

With oil and gas providing up to 60% of the world’s energy mix, humans still require fossil fuels for transport, electricity and materials - for survival - even as other sustainable supplies increase. As such companies and governments more than ever need realistic, comprehensive forecasts from an independent source.

However, the world must also adapt and reduce its use of fossil fuels in a changing world. This website offers knowledge about geology, future supplies of oil and gas, and details of exploration and development activity within the industry. Using a range of on- and off-line data, and consistent methodology, globalshift.co.uk is a free store of forecast and historical production, drilling and other information.

Globalshift.co.uk wishes to encourage independent and realistic analysis of the future of oil and gas, unfettered by wishful thinking or dogma. The histories and forecasts are derived from a very large range of trusted sources, as well as some less rigorous or reliable ones. All the information is sense-checked and modified where deemed appropriate and may be estimated and interpolated where data are unavailable.

The Energy Shift

For many decades energy prices have been volatile at periods of ‘peak supply’ (a peak in oil production driven by supply, demand or both) which has controlled the focus and magnitude of oil and gas exploration and development activity. For example, in 2005 tight supplies as a result of a diminishing pot of conventional resources led to oil price rises which contributed to a global recession in 2008. This was followed by a dramatic increase in the exploitation of unconventional resources (oil sands, oil and gas from tight reservoirs, natural gas liquids and, briefly, biofuels) followed by a sharp fall in the oil price in the latter half of 2014.

Now, super-imposed on this volatility is the impact of increasing environmental concerns about global warming and its effects on the climate. In this scenario energy price volatility is here to stay until the Energy Shift occurs.

The impact of peak supply has been to spur development of alternatives. However, peak supply (along with peak demand - collectively called peak oil) is poorly defined and often misunderstood. ‘Peak oil’ is not a single event, driven by a single cause. It is complex and evolving, depending on a variety of linked constraints.

Globalshift instead uses the term Energy Shift to encompass all that peak oil was once used to describe. It is hoped that, with proper planning, the Energy Shift will cause as little disruption to global economic activity as possible.

The Energy Shift is not - a signal of the end of exploration and discovery of oil and gas (or the end of drilling). The world finds new reserves every year. However, it may not find and produce enough to fully offset the decline in output from older finds.

An Energy Shift is not - the same as running out of, or abandoning, fossil fuels. We will not do this for a long time. The rate of oil (and then gas) production will simply cease to rise, plateau for a period, and then begin a slow and erratic decline.

An Energy Shift is not - necessarily a disaster for the fossil fuel industries. There are regular appearances of new opportunities in, for example; deep waters, oil sands, fractured shales, and manufactured alternatives, while conventional oil and gas types become more challenging and expensive to find and exploit. But ignoring it will cause more disruption than preparing for it (by investing in alternatives) especially as most alternatives have a lower power density.

An Energy Shift is not - a move to 100% renewables. Although this is inevitable in the long term (to conserve a stable environment for humans to live in), an Energy Shift only points to a steady and escalating growth in the use of renewables as fossil fuel availability reduces whilst prices rise, through market forces or by direct political action to reduce their use.